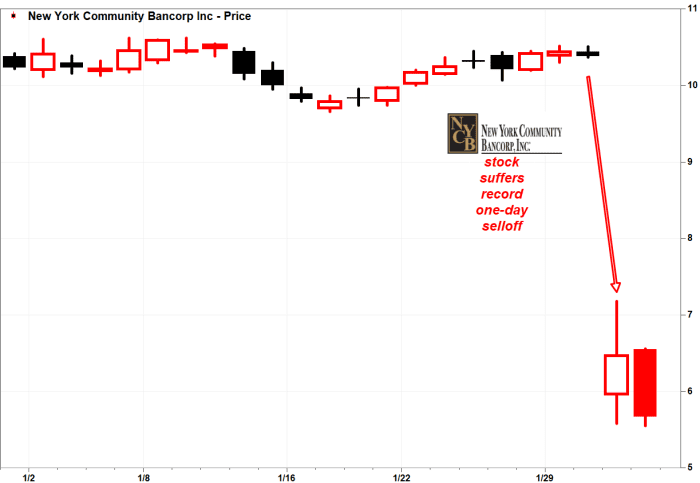

New York Community Bancorp Inc.’s stock on Thursday triggered the steepest drop in regional-bank stocks since the collapse of Silicon Valley Bank in March 2023, though the sector rebounded from earlier lows by the end of the session. .

New York Community Bancorp’s stock

NYCB,

In after-hours trading, the stock was up by 0.2%.

The bank’s swoon weighed on the financial sector, with the SPDR S&P Regional Banking ETF KRE down by 3.1% and the KBW Bank Index BKX off by 1.7%. The Financial Select Sector SPDR ETF XLF rose by 0.2% as the broad market rallied.

Earlier, the KRE index fund had been down by 10.9% over the previous two days — the biggest two-day selloff since it tumbled 16.2% over the two sessions ended March 13, 2023, on the heels of the collapse of Silicon Valley Bank.

Investor Chris Whalen, chairman of Whalen Global Advisors, said New York Community Bancorp should have done a better job in getting the news out about its disappointing fourth-quarter results, but noted his firm remains an owner of the stock.

“We still like the NYCB story and, indeed, bought more shares at the lows,” Whalen said in a post on his website. One notable data point for the bank was its fourth-quarter drop of 33% in unrealized losses on securities to less than 5% of capital, “partly as a result of aggressive sales of legacy securities and partly due to lower interest rates,” Whalen said.

The trouble for New York Community Bancorp began early Wednesday, when it posted a surprise loss and cut its dividend, sending its shares down by 37% for their largest one-day drop ever. The bank slashed its dividend to 5 cents a share, from 17 cents a share previously, and also took a $185 million loss on two loans, including an office-building loan.

While some on Wall Street have said the issues appear to be contained to the bank’s specific challenges to meet capital requirements, investors seem to be betting that New York Community Bancorp’s problem with one office loan could trigger losses at other lenders.

The office-space situation has been at the forefront as workers remain at home and the value of office-property loans potentially weighs on regional banks with exposure to harder-hit markets such as San Francisco, Washington, D.C., and New York City.

At the closing bell, Western Alliance Bancorp

WAL,

Valley National Bancorp

VLY,

Zions Bancorp

ZION,

Macrae Sykes, portfolio manager of the Gabelli Financial Services Opportunities ETF GABF, said the drop in financial stocks amounts to an opportunity to buy larger banks.

“We believe this real-estate impact will be material to the smaller/regional banks and disproportionately less impactful to the major banks due to lower concentration, sophisticated risk management and more conservative reserves,” Sykes said in an email.

Citi banking analyst Keith Horowitz said New York Community Bancorp’s results “were much worse than even the most bearish outlook,” but that the issues with the lender are “isolated” with “no read-through to other names.”

Moody’s Investors Service has placed all long-term and short-term ratings and assessments of New York Community Bancorp and its Flagstar Bank unit on review for a downgrade from its current rating of stable, the ratings agency said late Wednesday.

Moody’s cited the bank’s “unanticipated loss content in its New York office and multifamily properties, weak earnings, material decline in its capitalization and high and growing reliance on wholesale funding.”

While the bank’s acquisition of selected assets of Signature Bank improved its capitalization and funding profile, the same metrics deteriorated to pre-acquisition levels as of Dec. 31, partly because the bank now must meet Category IV regulatory requirements of being a bigger bank with $100 billion to $250 billion of assets, Moody’s said.

Moody’s said it “expects capitalization and funding to remain under pressure.”

After the close of trading on Wednesday, New York Community Bancorp said it expects 2024 net interest income of $2.8 billion to $2.9 billion, which is ahead of the FactSet consensus estimate of $2.76 billion.

Net interest income reflects a bank’s profit from loans minus money it pays out in the form of interest for savings accounts.

Crunching the new numbers, Wedbush analyst David J. Chiaverini reiterated his underperform rating on New York Community Bancorp, but said its new net interest income outlook is above his prior forecast of $2.7 billion.

Wedbush raised its 2024 earnings-per-share estimate for New York Community Bancorp to 80 cents a share from 65 cents a share, “owing mainly to higher average earning asset and net interest income assumptions following the company’s guidance update.”

Wedbush’s underperform rating on New York Community Bancorp is based on the bank’s above-average commercial real-estate exposure and the risk posed as these loans mature or reset and reprice at higher rates, he said.

Jefferies analyst Casey Haire downgraded New York Community Bancorp to hold from buy, and cut the bank’s price target to $6 a share from $13 on the bank’s unexpectedly fast Category IV bank compliance.

He cut his 2024 profit estimates for the bank by about 30%.

“NYCB’s actions taken thus far are a solid step forward, but impair profitability significantly given a need to run with higher capital/liquidity/reserves while trailing Cat IV peers modestly,” Haire said. “We expect the path to improved profitability will take years while credit risk remains an overhang.”

Raymond James analyst Steve Moss downgraded New York Community Bancorp to market perform from strong buy because its outlook changed unexpectedly.

“The announced repositioning significantly reduces the benefit of acquiring Signature Bank from the FDIC and highlights that regulatory rules for crossing $100 billion in assets is considerably more punitive, especially given the dividend cut and level of reserve build that occurred this quarter,” Moss said.

Along with its net interest income projection, New York Community Bancorp said it expects net interest margin of 2.4% to 2.5% — below the analyst estimate of 2.55%. However, its outlook includes actions to increase its balance-sheet liquidity and regulatory compliance.

It’s also projecting loans to drop by 3% to 5% in 2024, while its deposits are expected to increase by 3% to 5%.

The bank expects cash and securities to increase by $7.5 billion on a combined basis in 2024.

Also read: Banks’ office-loan exposure remains a ‘mixed bag’ as lenders manage through downturn

Tomi Kilgore contributed to this story.